English

/

Crypto Exchange April Recap

Share:

April 2026 continued the broader cooldown across crypto trading volumes, with Spot CEX, Futures, and Perp DEX activity all remaining below previous peak levels. In this recap, we break down how trading volumes evolved across centralized spot exchanges, futures markets, and onchain perpetual DEXs throughout the month, while also comparing current activity with previous cycle highs and longer-term market structure trends.

May 19, 2026

5 min read

by CryptoRank

CryptoRank

Share:

Key Takeaways

April 2026 continued the broader cooldown across crypto trading volumes, with Spot CEX, Futures, and Perp DEX activity all remaining below the elevated levels seen during the Q4 2025 rally. While derivatives continued dominating overall trading activity, volumes across both centralized and decentralized venues stayed noticeably lower compared to late 2025.

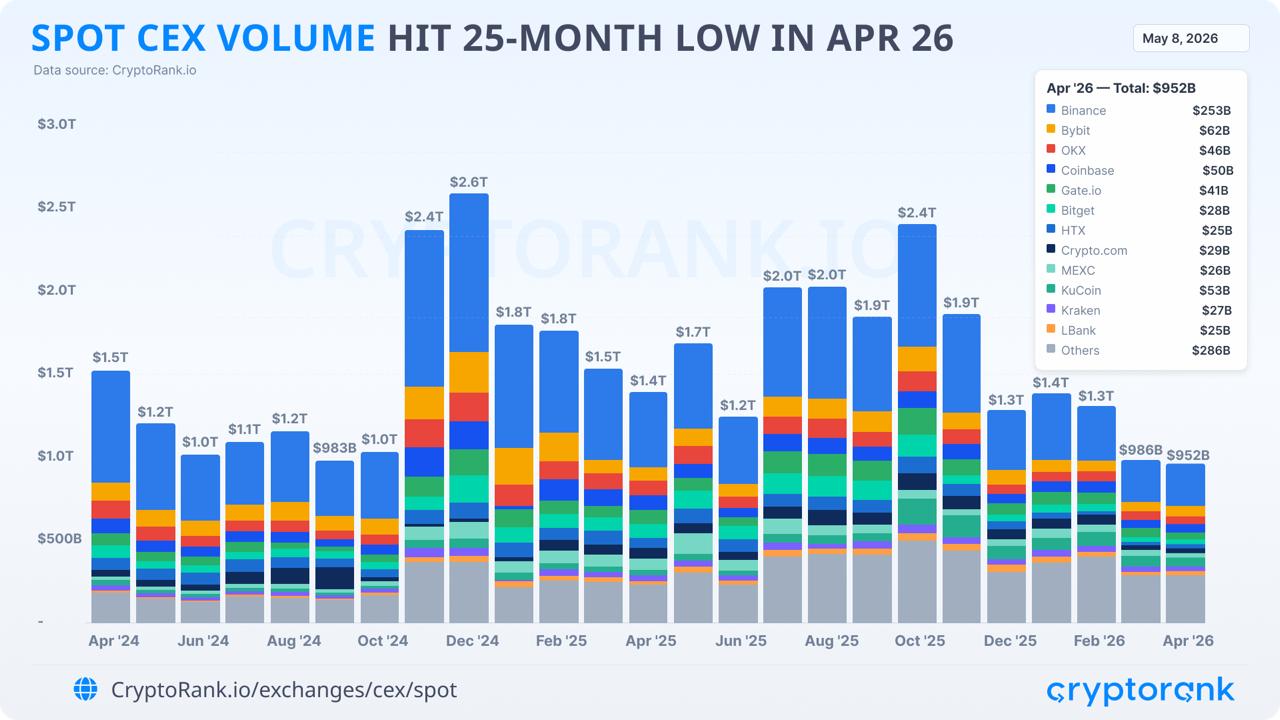

Spot CEX Total Volume: Falls to 25-Month Low at $952B

April 2026 marked another weak month for centralized exchange spot trading activity, with total CEX spot volume falling to $951.8B — down 3.5% from March’s $986B and now 63% below the December 2024 peak of $2.6T. The continued slowdown reflects the broader low-volatility environment across crypto markets throughout 2026.

Binance retained its clear lead with $252.6B in monthly spot volume and a 26.5% market share, remaining roughly four times larger than its nearest competitor. Coinbase was one of the strongest movers during the month, overtaking OKX to enter the global top four for the first time in over a year, while KuCoin continued holding third place.

Top 10 CEXs by April 2026 Spot Volume

-

Binance: $252.6B (26.5%)

-

Bybit: $62.0B (6.5%)

-

KuCoin: $53.3B (5.6%)

-

Coinbase: $50.4B (5.3%)

-

OKX: $46.1B (4.8%)

-

Gate.io: $41.3B (4.3%)

-

Crypto.com: $28.7B (3.0%)

-

Bitget: $28.4B (3.0%)

-

Kraken: $27.3B (2.9%)

-

MEXC: $26.3B (2.8%)

Among mid-tier exchanges, Gate.io continued outperforming relative to peers, holding 6th place with $41.3B in monthly volume and 4.3% market share. The exchange also maintained one of the industry’s broadest spot markets, listing 1,851 active trading pairs during April — the second-highest count among major CEXs.

Another notable trend was the growing compression among mid-sized exchanges. Platforms ranked between 6th and 12th place were separated by only around $16B in monthly volume, highlighting increasingly tight competition outside the top-tier venues. Meanwhile, HTX continued its gradual decline and fell out of the global top 10 as trading activity remained well below its 2024 levels.

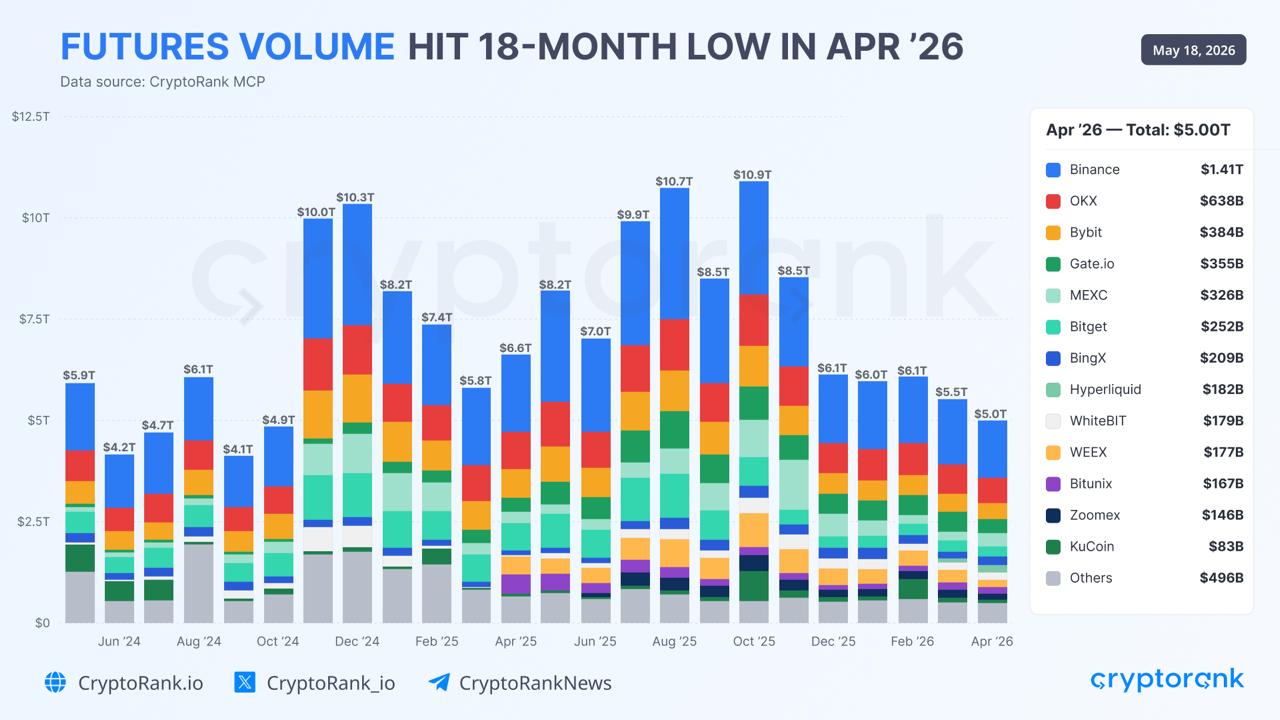

Futures Total Volume: Hits 18-Month Low at $5.0T

April 2026 futures trading volume declined to $5.0T, down 9.6% from March and marking the lowest monthly level since October 2024. Despite the continued cooldown, the pace of decline has started to stabilize compared to the sharp deleveraging seen immediately after the Q4 2025 peak.

Following the all-time high of $10.9T in October 2025, futures activity collapsed by 22% in November and another 28% in December. Since then, monthly declines have flattened to a steadier ~9% range, suggesting that the aggressive unwind phase may be slowing.

Top 10 Exchanges by April 2026 Futures Volume

-

Binance: $1.41T (28.2%)

-

OKX: $638B (12.8%)

-

Bybit: $384B (7.7%)

-

Gate.io: $355B (7.1%)

-

MEXC: $326B (6.5%)

-

Bitget: $252B (5.0%)

-

BingX: $209B (4.2%)

-

Hyperliquid: $182B (3.6%)

-

WhiteBIT: $179B (3.6%)

-

WEEX: $177B (3.5%)

Competition below the market leaders remained relatively dense in April. Exchanges outside the top three — from Gate.io to WEEX — all operated within a fairly narrow $177B–355B monthly volume range, showing that the mid-tier futures market remains highly competitive despite the broader slowdown in trading activity.

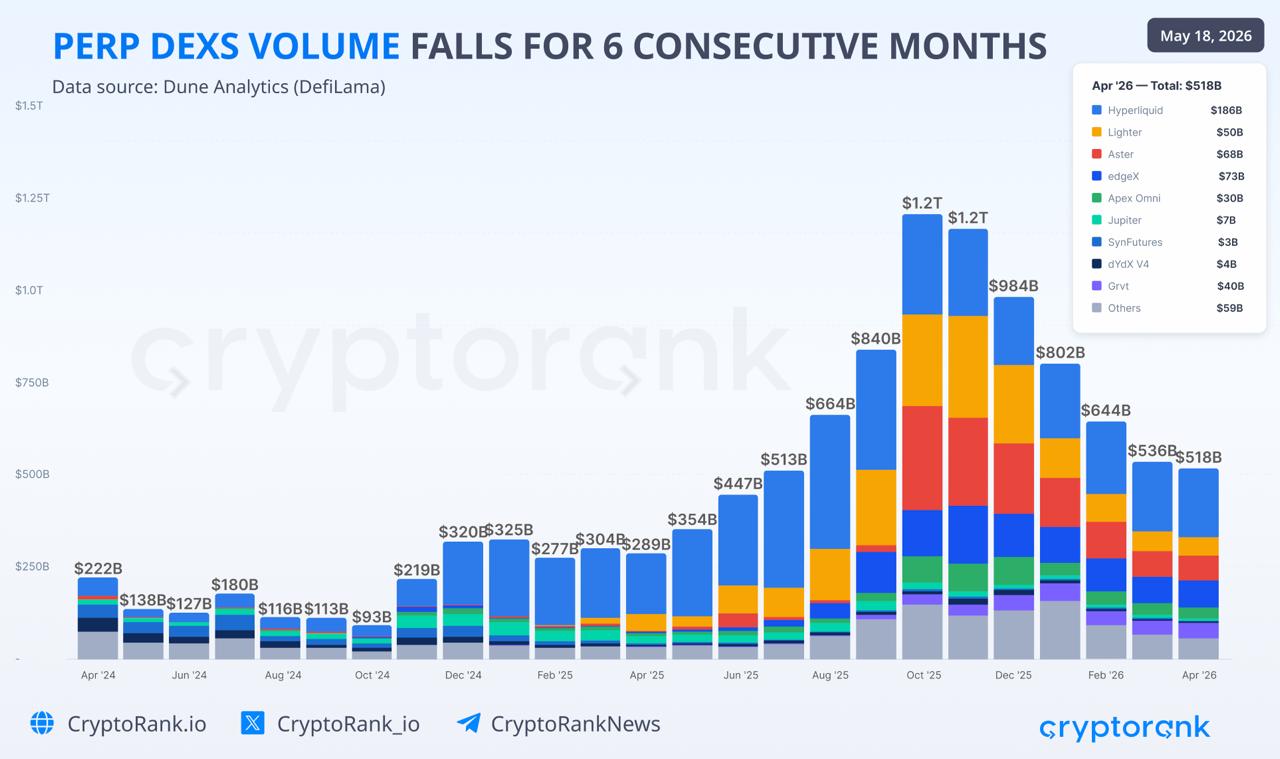

Perp DEX Total Volume: Falls to $518B After 6 Consecutive Monthly Declines

Perp DEX trading volume declined to $518B in April 2026, down 3% from March’s $536B. While activity continues cooling after the Q4 2025 breakout, April marked the smallest monthly decline since the October 2025 peak of $1.2T.

Following the sharp contraction earlier this year — from $802B in January to $644B in February and $536B in March — the pace of decline has noticeably slowed. Total Perp DEX volume now sits roughly 57% below its peak, though recent data suggests the broader deleveraging phase may be stabilizing.

Top 9 Perp DEXs by April 2026 Volume

-

Hyperliquid: $186B (35.9%)

-

edgeX: $73B (14.1%)

-

Aster: $68B (13.1%)

-

Lighter: $50B (9.7%)

-

GRVT: $40B (7.7%)

-

ApeX Omni: $30B (5.8%)

-

Jupiter: $7B (1.4%)

-

dYdX V4: $4B (0.8%)

- Others: $59B (11.4%)

Hyperliquid remained the dominant platform by a wide margin, generating $186B in monthly volume and accounting for nearly 36% of total Perp DEX activity. Despite the broader cooldown, newer platforms such as edgeX, Aster, and Lighter continued holding meaningful market share and remained among the largest onchain derivatives venues by trading activity.

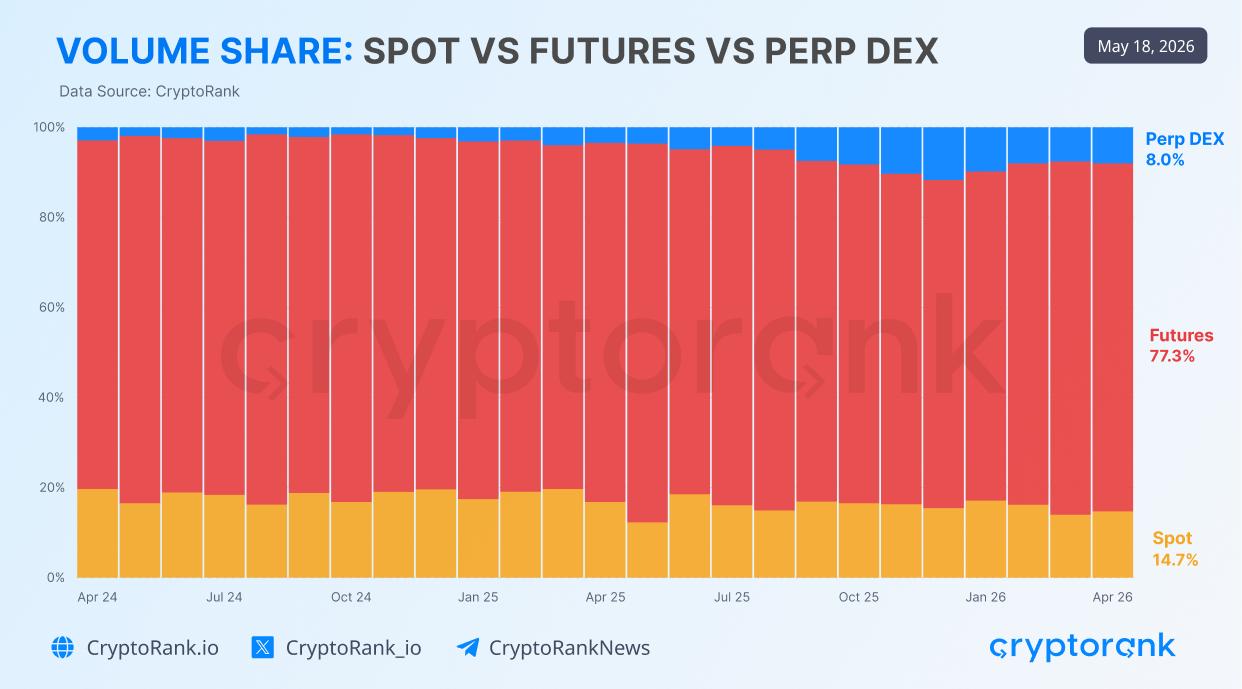

How Spot, Futures and Perp DEX Share the Market

Looking at the breakdown over the past two years, one trend stands out: the rise of decentralized perpetuals.

In April 2024, Perp DEX accounted for just 2.9% of total trading volume. Spot held a steady 19.7%, and Futures dominated with 77.4% – roughly the same split the market had run on for years.

Fast-forward to April 2026, and the picture has shifted:

-

Perp DEX → 8.0% (up from 2.9%, nearly tripling its share)

-

Spot → 14.7% (down from 19.7%)

-

Futures → 77.3% (essentially unchanged)

Worth noting where the change actually came from. Futures held its position. Perp DEX didn't take volume from centralized derivatives; it took it from Spot. Retail and active traders who used to buy and hold on CEX spot markets are increasingly opening leveraged positions on-chain instead.

Post-Peak Dynamics: Where the April Numbers Place Us in the Cycle

Zooming out to the October 2025 peak, all three segments have given back roughly half of their cycle gains:

-

Spot: $2.4T → $952B (−60%)

-

Futures: $10.9T → $5.0T (−54%)

-

Perp DEX: $1.2T → $518B (−57%)

The fact that all three contracted in lockstep — and by similar magnitudes — points to a single market-wide cycle rather than segment-specific weakness.

April was the calmest month for trading volumes since the October peak. All three segments dropped by less than 10% — Perp DEX cooled from four straight months around −18% to just −3.4%, Spot bounced back from March's −24% drop to −3.4%, and Futures held its post-crash range around −9.6%, far from the −22% and −28% crashes seen in November and December. Whether this is a base being built ahead of the next leg up or just a pause before further decline will become clearer over the next few months.

Disclaimer: This post was independently created by the author(s) for general informational purposes and does not necessarily reflect the views of Algona Business Ltd. The author(s) may hold cryptocurrencies mentioned in this report. This post is not investment advice. Conduct your own research and consult an independent financial, tax, or legal advisor before making any investment decisions. The information here does not constitute an offer or solicitation to buy or sell any financial instrument or participate in any trading strategy. Past performance is no guarantee of future results.

Without the prior written consent of CryptoRank, no part of this report may be copied, photocopied, reproduced or redistributed in any form or by any means.