Why Institutional Adoption Depends on Better On-Chain Infrastructure

Share:

Share:

Key Takeaways

-

Institutional crypto adoption is shifting from speculation to infrastructure-building, treating digital assets as financial plumbing rather than just a trade.

-

For order-book-based chains, revenue and TVL are decoupling, which makes TVL an increasingly unreliable signal of how much real economic activity a chain supports.

-

Native, canonical stablecoin issuance is becoming a competitive edge for blockchains courting institutional liquidity, not just a convenience feature.

-

Crypto's regulatory path is getting more systematic and less case-by-case, but access still has to convert into volume that sticks, and that part remains unproven.

Institutional Finance Is Moving On-Chain

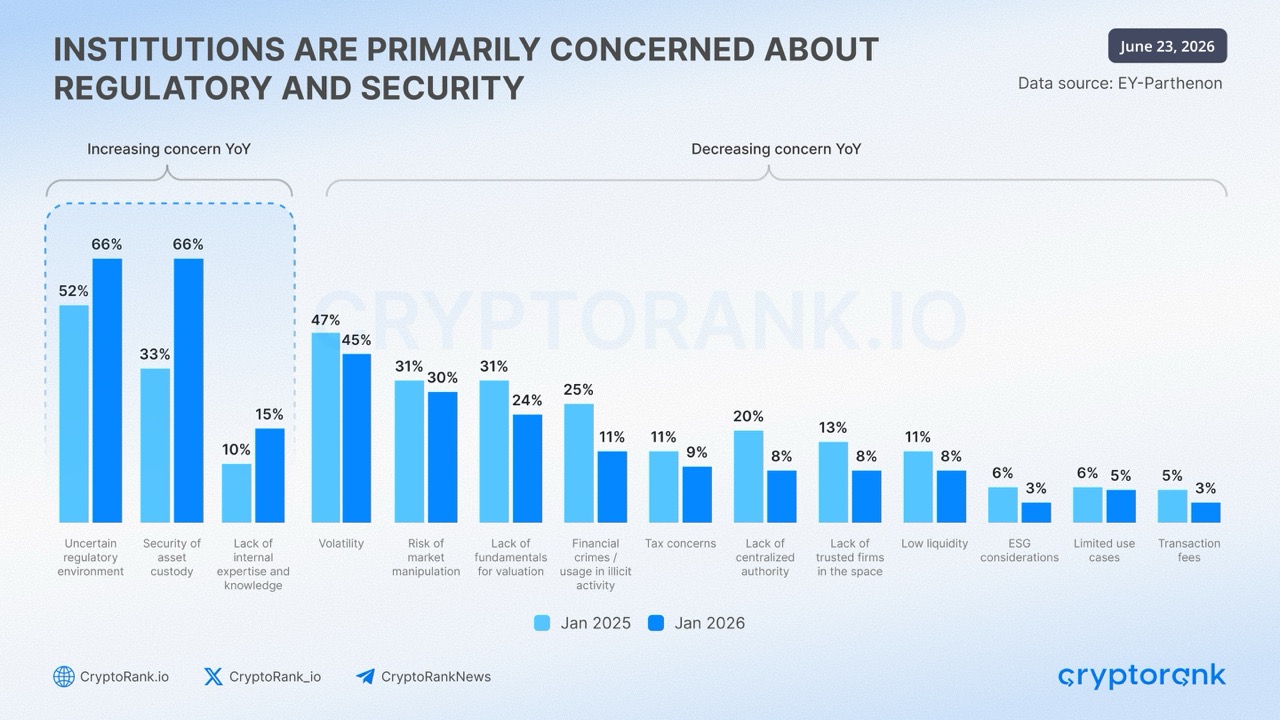

Institutional crypto adoption is shifting from simple asset exposure toward broader use of blockchain infrastructure. A recent EY-Parthenon and Coinbase survey of more than 350 institutional investors found that 73% planned to increase their digital asset allocations, with trading, custody, and tokenization the most common capabilities firms are building out.

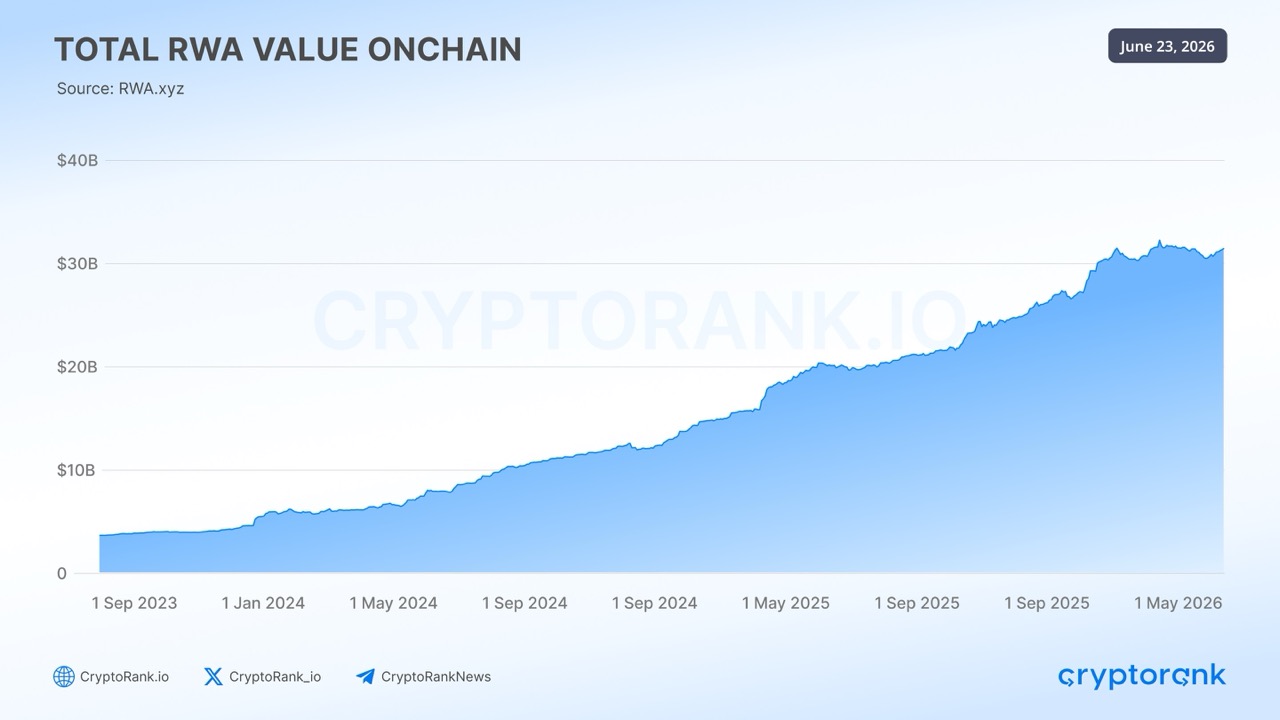

The market data backs this up. By June 2026, tokenized assets on-chain had reached roughly $31.6 billion, and the stablecoin market had grown past $300 billion. Among the surveyed institutions, 86% were already using stablecoins or actively exploring them, mostly for T+0 securities settlement, internal cash management, and continuous trading.

Institutions are starting to treat blockchains as infrastructure for issuance, trading, and settlement, not just as a way to get exposure to crypto assets. The open question is whether decentralized systems can match what institutional-scale finance actually needs, such as liquidity, reliability, regulatory controls, and operational convenience.

What Institutions Require from On-Chain Infrastructure

Moving financial activity on-chain takes more than fast transactions and low fees. Institutions need regulated access, secure custody, predictable execution, and the ability to plug into the systems they already run.

Settlement is another core requirement. Financial assets need a cash instrument that’s trusted, liquid, and capable of completing transactions with clear finality. Ideally, the asset and the payment move at the same time, which cuts down on counterparty exposure and the need for reconciliation. A BIS research report places reliable settlement money and atomic delivery-versus-payment at the center of tokenized financial infrastructure.

Liquidity also needs to move freely across networks and applications. Right now, assets and capital are split across blockchains, private ledgers, custodians, and traditional market systems. DTCC argues that this fragmentation drives up operational costs and limits liquidity, asset mobility, and fungibility. True interoperability means covering token transfers as well as ownership records, settlement, corporate actions, collateral, and regulatory reporting.

Institutions also expect blockchain systems to keep the controls that traditional markets already have, including legal certainty, data privacy, compliance checks, asset safeguarding, and resilience when activity spikes. At the same time, they want to keep blockchain’s advantages: continuous markets, programmable transactions, faster settlement, and more efficient use of collateral.

This is the opening that finance-focused public blockchains are trying to fill. General-purpose networks are bolting on institutional settlement, tokenization, and compliance features as they go, while finance-focused chains build them into the base layer from the start. Injective takes the second approach, combining trading infrastructure, settlement rails, tokenized markets, and application execution in one network.

Injective: A Layer 1 Built for Financial Markets

Injective is a public Layer 1 blockchain built specifically for on-chain financial applications. Since November 2025, Injective has run as a MultiVM network, letting EVM and WASM applications share assets, liquidity, and state. It has roughly 650-millisecond block times, deterministic finality, throughput up to 25,000 transactions per second, and fees that are close to nothing.

|

Metric |

Value |

Source / as of |

|---|---|---|

|

Protocol revenue rank (trailing 12m) |

#10 of all L1s ($3.34M) |

Token Terminal, Jun 2026 |

|

Derivatives volume settled (Jan 2025 to 6/21/26) |

$33.9B (crypto ~80% / RWA ~20%) |

Injective |

|

RWA trading volume, cumulative (Jan 2025 to 6/21/26) |

$6.8B |

Injective |

|

Total value locked |

~$10.7M |

DefiLlama, Jun 2026 |

|

Monthly active users |

~135K (+40% YoY) |

Token Terminal, Jun 2026 |

|

INJ burned via buyback, since 2021 |

7,106,386 INJ / $36,490,707 |

Injective Hub |

|

MultiVM (Native EVM) launch |

November 11, 2025 |

Injective |

Source: Token Terminal, DeFiLlama, Injective; as of June 21, 2026

Where Injective Stands in Broader L1 Landscape

The case for Injective as a settlement layer is strongest where the numbers are hardest to argue with. Over the trailing twelve months, Injective ranks as the tenth-highest-earning Layer 1 by protocol revenue at $3.34 million, just behind Internet Computer and ahead of most of the field.

Top 10 Layer 1 Blockchains by 12M Revenue

|

Rank |

Layer 1 |

Revenue (trailing 12m) |

|---|---|---|

|

1 |

Tron |

$3.12B |

|

2 |

Ethereum |

$121.9M |

|

3 |

Solana |

$38.5M |

|

4 |

BNB Chain |

$22.3M |

|

5 |

Polygon |

$11.4M |

|

6 |

Avalanche |

$6.7M |

|

7 |

Sui |

$5.5M |

|

8 |

NEAR Protocol |

$5.1M |

|

9 |

Internet Computer |

$3.35M |

|

10 |

Injective |

$3.34M |

Source: Token Terminal, as of June 9, 2026

And it earns that revenue while tying up almost no capital. At roughly $10.7 million, Injective’s TVL is among the smallest of any major DEX, even though the chain has cleared tens of billions in cumulative volume. That low number reflects how the venue works, not how much activity it sees: Injective’s central limit order book draws depth from a network of professional trading firms and institutions rather than from capital parked in AMM pools, so volume and revenue are the numbers that actually describe the design, not TVL.

Nearly all of that revenue flows back to the token. Through the Community BuyBack, participants commit INJ and get a pro-rata share of real ecosystem revenue in return, while the INJ they put in gets burned permanently. Since 2021, this mechanism has removed more than 7.1 million INJ, worth about $36.5 million, and it’s currently running at close to 567,000 INJ a year. By design, the burn rate climbs as the ecosystem generates more revenue. Meanwhile, monthly active users, now around 135,000, are up roughly 40% over the past year.

The Finance-Native Base Layer

Injective’s main distinction is how much financial infrastructure sits inside the protocol itself, rather than being left to application developers. A central limit order book that matches orders on-chain, block construction designed to resist MEV, and sub-second finality at fees that round down to a fraction of a cent are all built in from the start.

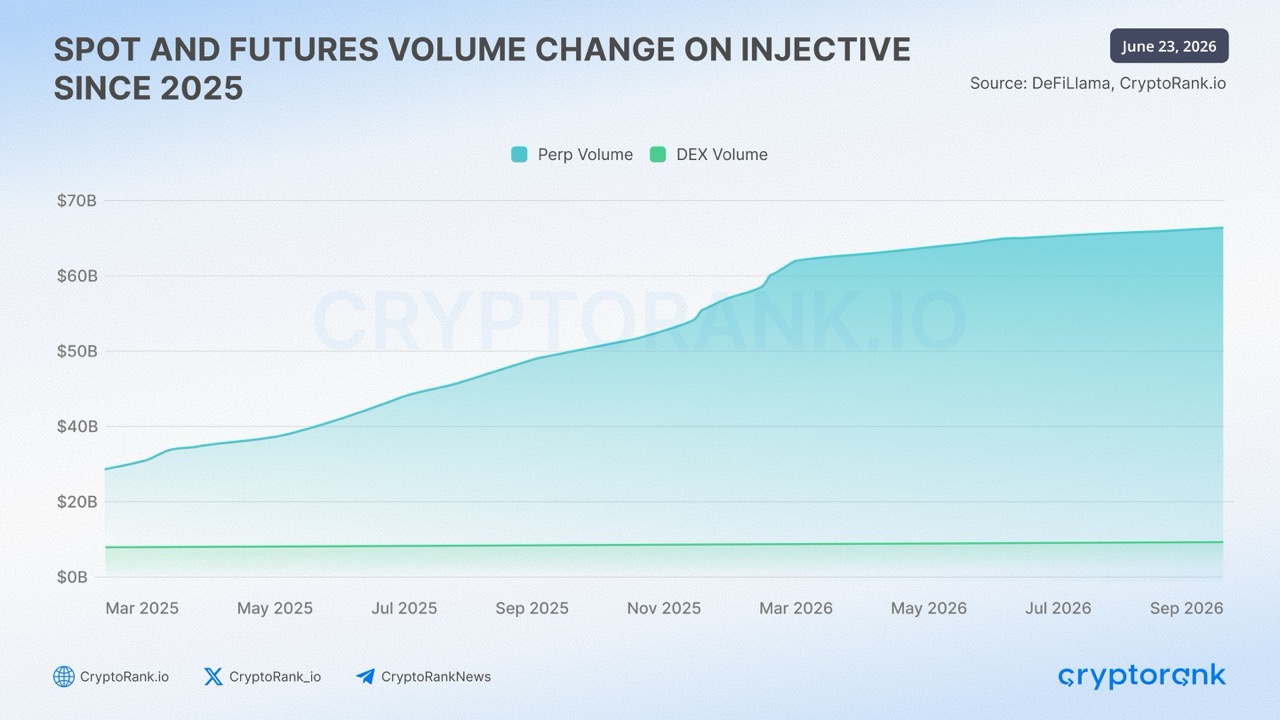

That base is already moving real size. Since January 2025, Injective has cleared roughly $33 billion in derivatives volume, about 80% of it crypto spot and perpetual trading, with real-world assets making up the rest. The stablecoin rails, the RWA markets, and the regulated access described below all plug into this trading core.

Four Layers of Injective’s On-Chain Economy

Four pieces make up Injective’s on-chain economy: stablecoin settlement, trading infrastructure, application execution, and institutional access, all running on shared liquidity and state.

The Stablecoin Layer: Native USDC and Settlement Rails

A settlement layer needs something to settle in. On May 7, 2026, Injective got native USDC alongside Circle’s canonical CCTP V2, with Circle issuing the coin directly on-chain, fully backed and redeemable one-for-one, with no bridging and no wrapped stand-in required. Because Injective shares state across its virtual machines, that USDC holds a single balance spanning both the EVM and WASM sides, so liquidity doesn’t fracture between execution environments.

Uptake came fast. Helix, the network’s flagship exchange, saw its liquidity climb more than 40% after the launch. Within four days, Cosmos Hub had named Injective-issued USDC its primary standard, and dYdX started shifting onto it under a multi-year arrangement. The Vulcan upgrade in June tightened the standard further, adding stricter metadata rules for every asset minted through the chain’s token factory. What matters here isn’t the opening-day balances so much as which venues are choosing Injective-issued USDC as their canonical rail.

The Regulated-Access Layer: Futures and the ETF Path

Institutions also need a regulated way in. On April 15, 2026, Bitnomial, a CFTC-regulated designated contract market, listed the first US-regulated INJ futures. That puts INJ in the same regulated-futures category as BTC, ETH, SOL, and XRP. It also starts a clock: the SEC’s generic listing standards for commodity-based ETPs, cleared on September 17, 2025, let six months of regulated futures trading open an ETP listing path without a case-by-case review, which puts the earliest qualifying date at October 15, 2026.

Three INJ ETF applications are already on file, from 21Shares, Canary Capital, and REX-Osprey. Injective has paired that market access with a policy push of its own: it set up the Injective Policy Institute in Washington, D.C., and joined the Blockchain Association. That combination (live regulated futures, pending ETF filings, a generic listing framework already in force, and dedicated advocacy) isn’t common. An approved ETF would open a passive-capital channel that INJ doesn’t have today.

The RWA Layer: From Infrastructure to Markets

Injective’s real-world-asset plumbing isn’t new. The native RWA module arrived with the January 2024 Volan upgrade, the RWA Oracle followed that August, and RWA perpetual futures went live in February 2025. Cumulative RWA trading volume now stands at $6.8 billion, split across asset classes like this:

|

RWA asset class |

Cumulative volume |

Share |

|---|---|---|

|

Equities |

$4.15B |

61% |

|

FX |

$977M |

14% |

|

Commodities |

$913M |

13% |

|

Indices |

$763M |

11% |

Source: Injective, as of June 21, 2026

Beyond perpetuals, the tokenized side includes some recognizable names. Pineapple Financial (NYSE: PAPL) has brought $1.2 billion on-chain across 2,079 mortgage records, with a stated goal of $10 billion across 29,000 mortgages. Institutional funds come in through Libre, the venture tied to Nomura’s Laser Digital, including the BlackRock Money Market Fund and the Hamilton Lane SCOPE Senior Credit Fund. Pre-IPO perpetuals on private companies such as OpenAI launched in late 2025 and sit in a separate category from the RWA figures above. Vulcan also pushed cheaper institutional-grade pricing into these markets and set up a planned Morpho integration that would carry Injective’s price feeds into on-chain lending and credit.

The Execution Layer: MultiVM and the Vulcan Upgrade

Underneath all of this sits the Native EVM mainnet, which shipped on November 11, 2025, the largest upgrade Injective has run. This turned the chain MultiVM: EVM and WASM now share one state, with tokens represented as a single canonical balance on both sides through the MultiVM Token Standard. Ethereum developers can bring their existing Solidity contracts and the development frameworks they already use, like Hardhat and Foundry, and connect directly to the native Exchange module, the RWA stack, and the shared liquidity layer, rather than rebuilding from scratch on generic rails.

Two upgrades have built on that base. IIP-619, the “Real-Time EVM” release that passed on February 19, 2026, sharpened the Chainlink oracle integration for live price feeds and widened the shared liquidity layer. The Vulcan mainnet upgrade, which went live in early June 2026, introduced a redesigned oracle engine that cuts oracle gas costs by about 90%, plus a new oracle precompile that hands canonical Injective price data straight to EVM contracts. The team is also exploring support for additional virtual machines.

Risks and Open Questions for Injective

The integrations is in place. What it still has to prove is durable activity. The common thread across every layer is conversion: do onboarded institutions, new stablecoin rails, and incoming EVM applications turn into volume that sticks around? Rival finance-focused and RWA Layer 1s are multiplying. Native USDC has to hold its ground against much larger USDC pools on Ethereum and Solana. The ETF timeline has to land on schedule rather than slip. And large RWA migrations, like Pineapple’s, move from origination to live on-chain markets only gradually. None of this is settled, and all of it will show up in the data over the next several quarters.

The Bottom Line

As institutions move on-chain, the challenge isn’t simply getting assets onto a blockchain anymore. Financial markets need reliable settlement, liquidity, execution, application infrastructure, and regulated access working together, and in most ecosystems today, those pieces are scattered across different chains, bridges, applications, and off-chain providers.

Injective’s model is more integrated. Once known mainly as a Cosmos-based derivatives chain, it has grown into a finance-native MultiVM Layer 1 with native stablecoin settlement, tokenized assets, regulated market access, and Ethereum-compatible execution all in one place. Pulling a top-ten Layer 1 revenue rank with relatively little capital locked up is a real signal of how efficient that model is. The numbers are still early, but the harder thing to copy is the architecture itself: several layers of on-chain finance running through one shared market.