Coinhold by EMCD: Fee-Based Yield on a Mining Ecosystem

Share:

Share:

Introduction

One of the more distinctive features of the crypto market is its capacity to generate yield across asset classes that are primarily known as speculative holdings. Bitcoin, stablecoins, and major altcoins can all be put to work, and a mature infrastructure has emerged on both sides of the market to make that possible.

The yield mechanics and rate ceilings differ meaningfully between the two. DeFi protocols are fully transparent by design, with rates set algorithmically against observable on-chain demand, but that transparency comes with a structural ceiling. CeFi platforms can reach institutional lending markets, OTC desks, and yield mechanisms that on-chain protocols cannot access directly, which is why their headline rates tend to sit higher. Visibility is the tradeoff. The yield arithmetic on the CeFi side is harder for depositors to verify independently.

This piece examines Coinhold, a savings wallet built on EMCD's mining ecosystem. The goal is to understand the yield mechanisms behind its rates, how those rates compare to the current market, and what the relevant risks and limitations are for depositors evaluating it.

The Ecosystem Behind the Product

EMCD launched in 2017 as a Bitcoin mining pool and has expanded over nine years into a multi-product crypto ecosystem. The mining pool itself ranks among the top seven globally by hashrate, and the broader platform now includes a custodial wallet, a zero-fee P2P marketplace, crypto-backed lending, and Coinhold as a savings wallet for the ecosystem users.

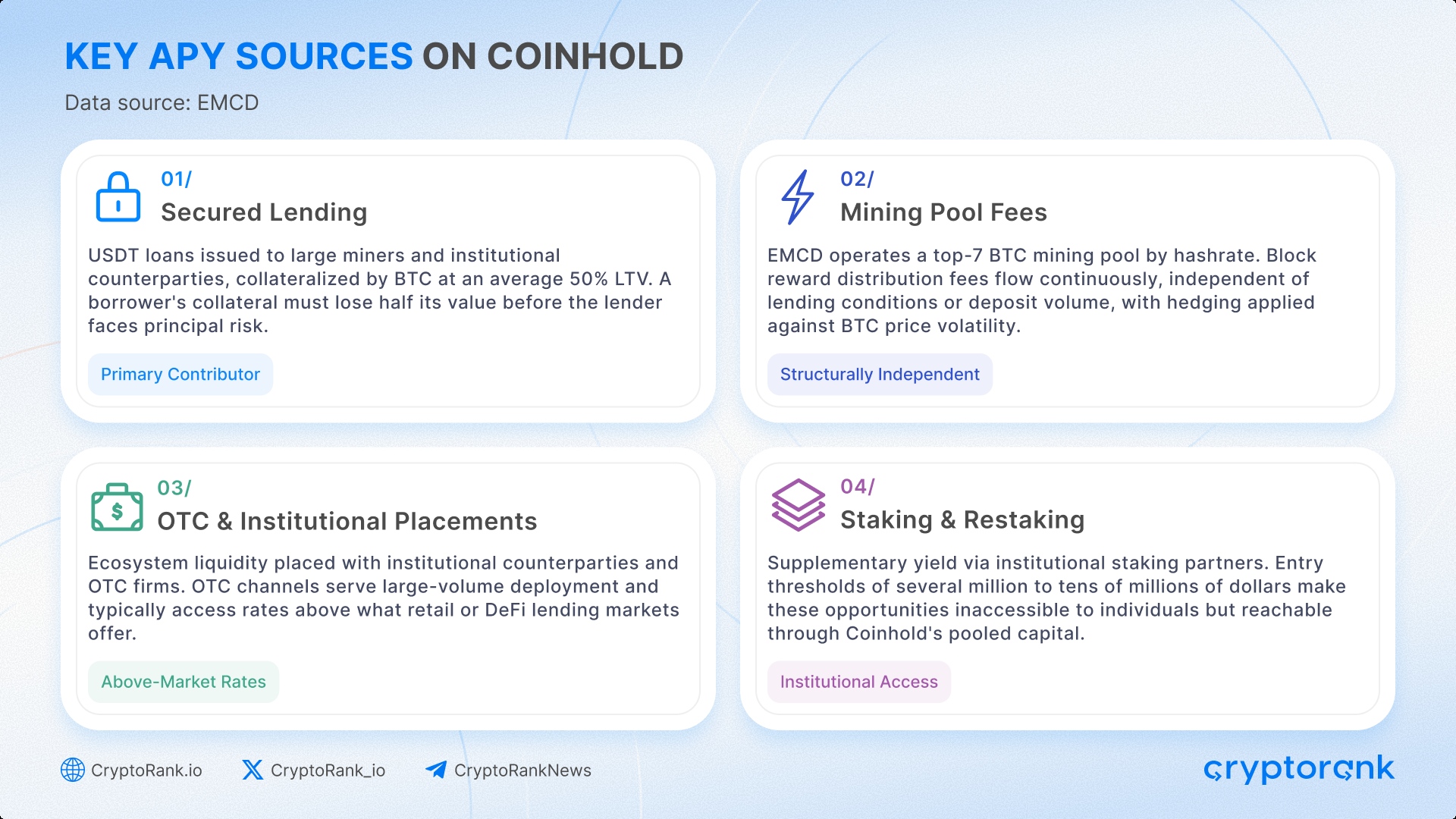

Most centralized lending platforms run on a single mechanism. They borrow depositor capital, deploy it at a higher rate, and return a portion of the spread. When that spread compresses, depositor yield is directly exposed. EMCD draws on four yield sources that operate independently of each other, each contributing to the overall rate.

One is secured lending against digital assets. EMCD issues USDT loans to large miners and institutional counterparties, collateralized by BTC at an average loan-to-value ratio of 50%. At that threshold, a borrower's collateral must lose half its value before the lender faces principal risk.

Running alongside that is fee income from the mining pool. Block reward distribution fees flow continuously and independently of lending market conditions, with hedging mechanisms in place to smooth out BTC price volatility. This is the component that most clearly separates Coinhold from a standalone lending product. It is a revenue base that does not depend on deposit volume or loan demand in any given period.

A portion of ecosystem liquidity is also placed with institutional counterparties and OTC firms. OTC transactions serve as the primary channel for large-volume deployment and typically access rates above what retail or DeFi lending markets offer.

The fourth stream is staking and restaking through institutional partners. EMCD notes that entry thresholds for such arrangements typically run from several million to tens of millions of dollars, placing them out of reach for individual depositors but reachable through the pooled capital Coinhold operates at scale.

The combination is what gives Coinhold's economics a different shape from a conventional lending platform. A lending spread augmented by mining fee income, institutional placement margins, and staking yield has a plausible arithmetic basis for producing returns above what a single-source lender can offer.

Custody Model and Yield Mechanics

Coinhold is a custodial product, which means that users' deposits are held on EMCD. However, these funds are held separately from company operational capital, and are not recorded on EMCD's corporate balance sheet as company assets. Funds are not rehypothecated under the platform's current liquidity and risk management framework.

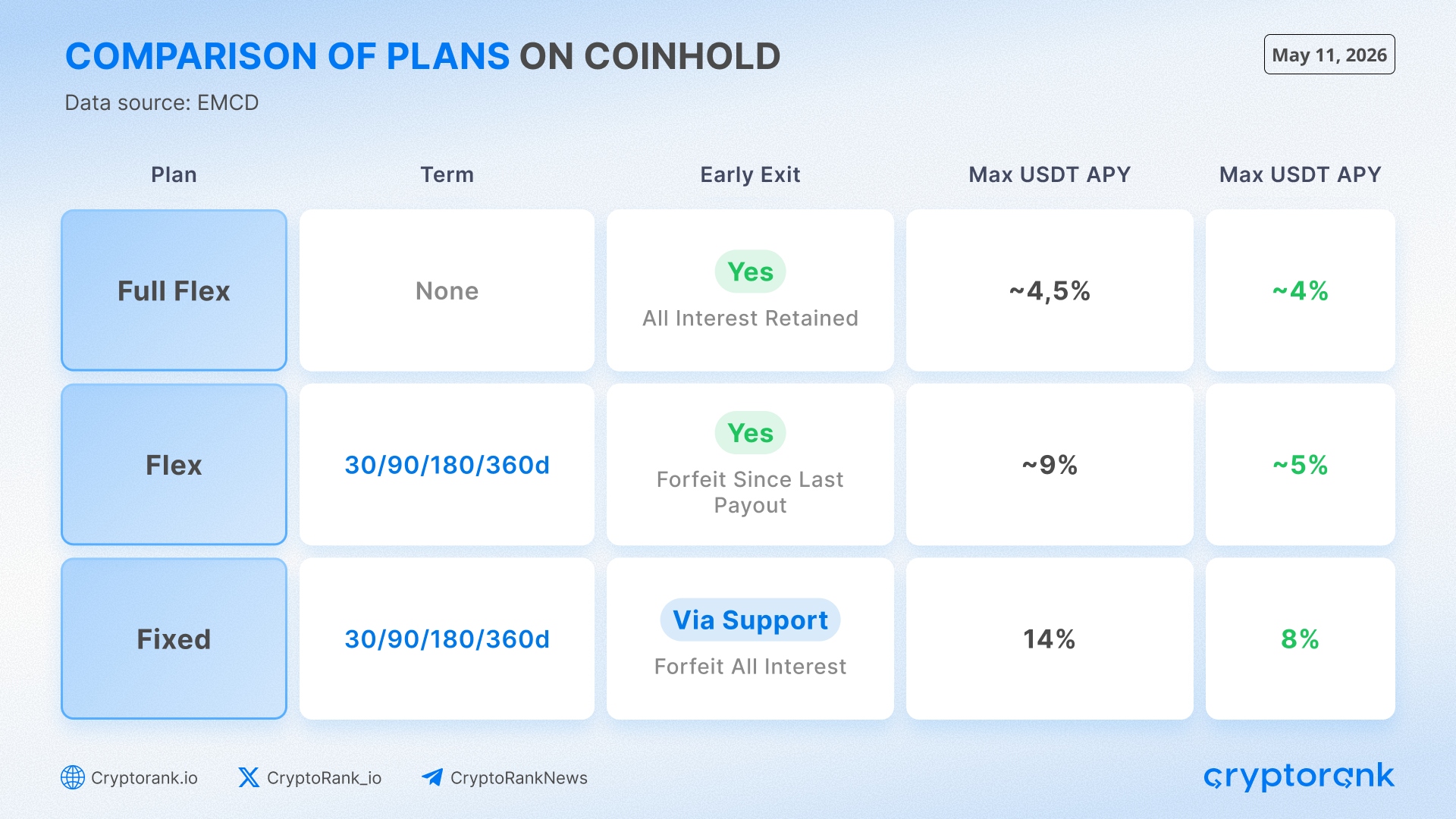

Coinhold offers three asset-saving formats with varying returns and withdrawal flexibility. The greater the withdrawal flexibility, the lower the returns, and vice versa.

Interest accrues daily across all plan types and is distributed every 30 days. By default, that interest compounds into the Coinhold balance rather than being paid out, which puts the effective rate up to 14.7%. For some plan types users can elect direct wallet payouts instead. All withdrawals outside scheduled maturities carry a 24-hour processing hold. Top-ups are permitted at any time under any plan with no restrictions.

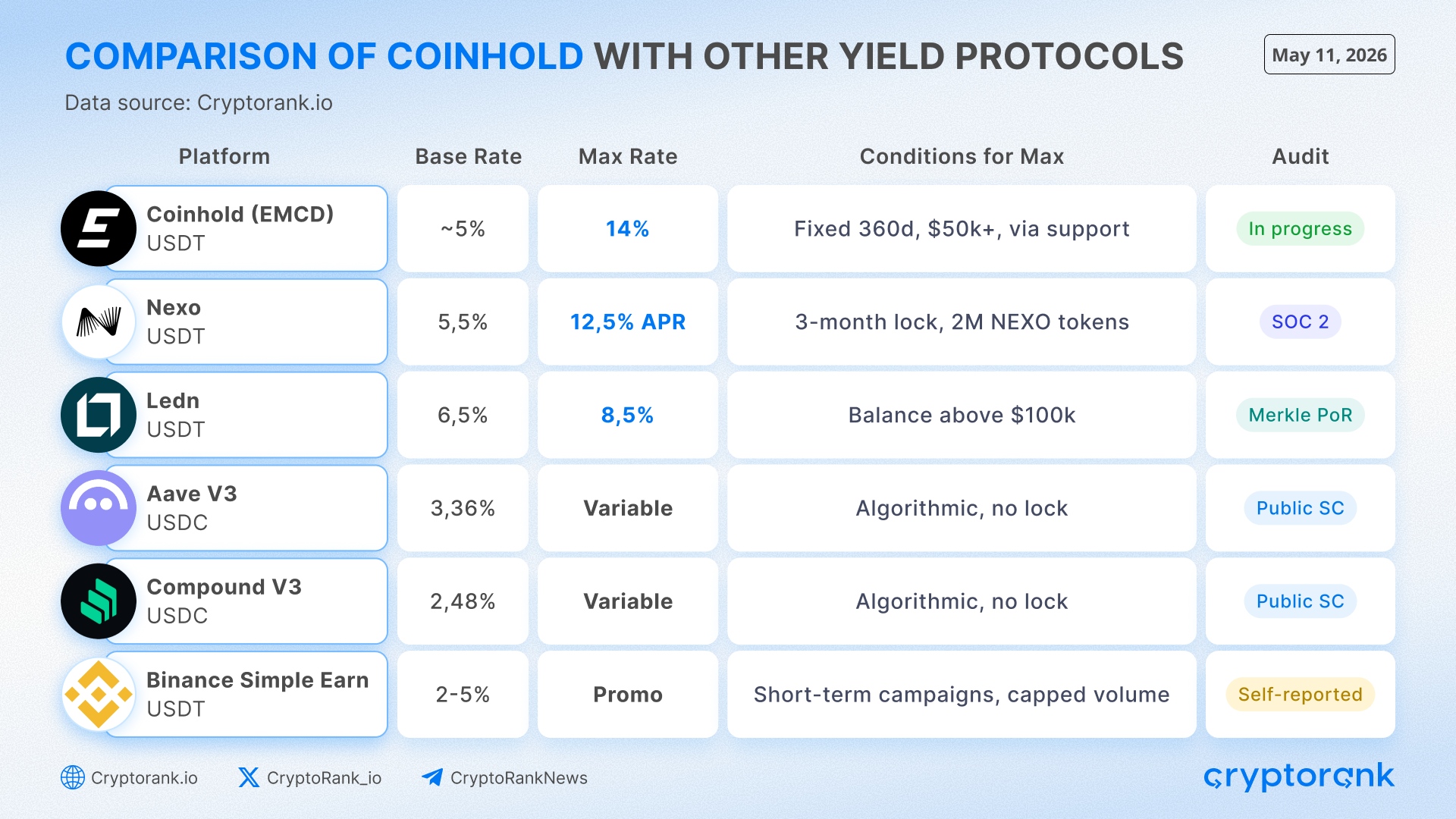

The 14% maximum rate on USDT applies under a specific set of conditions. It requires the Fixed plan, a 360-day term, a minimum deposit of $50,000, and confirmation through support. For standard retail-sized deposits, the effective Flex ceiling on USDT is approximately 9%.

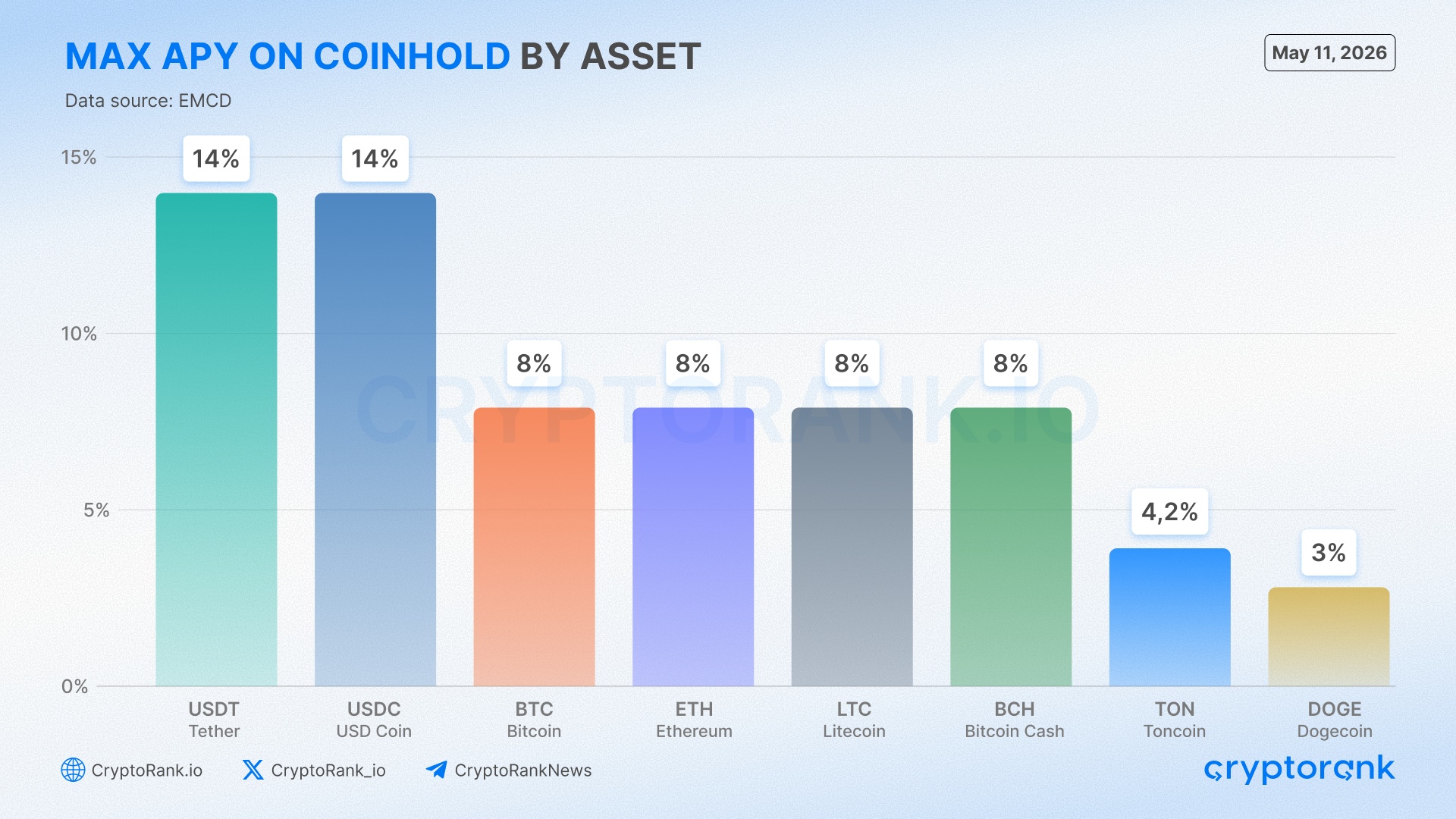

The APR differentiation across assets reflects deployability. USDT and USDC are the most liquid instruments in the BTC-backed institutional loan book, which generates the largest share of yield. BTC earns less because lending BTC directly produces lower spreaPrds than lending stablecoins collateralized by BTC. DOGE and TON sit at the lower end for the same reason: limited institutional borrowing demand for those assets constrains what the platform can generate from deploying them.

The auto-top-up feature deserves a separate note as a mechanics point. Miners on EMCD's pool can configure any percentage of their daily payouts to flow directly into Coinhold without any manual transfer step. This creates a continuous, low-friction funding channel between the pool and the savings product, reinforcing the closed-loop structure described in the previous section.

Yield Sources and Rate Comparisons

The gap between Coinhold's 14% USDT rate and the broader market is wide enough to warrant a closer look at what the competition actually produces and how.

DeFi lending protocols generate yield purely from borrowing demand, with depositor rates set algorithmically based on pool utilization in real time. Aave V3's USDC pool on Ethereum currently shows a supply APR of 5.55%, but that reflects a high-utilization event: the 30-day average sits at 4.27% and the 6-month average at 3.36%. Compound V3's USDC market on Ethereum is more representative of the structural floor, clearing 2.48% to 2.58% APY across recent daily snapshots. These rates are fully transparent and verifiable on-chain, but their ceiling is bounded by what borrowers on those platforms are willing to pay.

Centralized platforms access institutional lending markets that DeFi protocols cannot reach directly, which is why their rates tend to sit above that floor. Ledn offers 6.5% on the first $100K of USDT and 8.5% above that threshold, backed by quarterly proof-of-reserves reports. Nexo's base USDT rate is 5.5%, rising to 8.5% for balances above $100,000 at standard loyalty tiers. Its advertised maximum of 12.5% APR requires holding 2,000,000 NEXO tokens, locking assets for three months, and receiving interest in NEXO rather than the deposited asset. Binance Simple Earn's flexible USDT product operates in the 2% to 5% APR range under normal conditions, with periodic promotional boosts that are short-term and volume-capped.

Most CeFi platforms generate depositor returns by redeploying user capital into loans, money markets, or counterparty arrangements, then sharing a portion of the resulting spread. In that model, depositor yield is directly tied to how the platform manages that redeployment. A loan book that underperforms or a counterparty that defaults flows through to the depositor.

Mining pool fee income sits outside that structure. It is generated by operational activity, processing block rewards and charging distribution fees, and accrues regardless of lending conditions or deposit levels. The depositor is not exposed to a borrower's creditworthiness when yield comes from this source, only to the operational performance of a pool with a nine-year track record and an independently observable hashrate. The other yield components, lending, OTC placements, and staking, do carry counterparty exposure, but this portion does not.

Risk Assessment and Open Questions

The primary lending model is simple: users can get USDT without selling their BTC. They provide BTC as collateral and receive a loan equal to 50% to 90% of its value. For example, $10,000 in BTC can unlock $5,000 to $9,000 in USDT.

The more a user borrows against the same BTC, the smaller the safety buffer if the BTC price falls. If the collateral is no longer enough to safely cover the loan, EMCD closes the loan using the collateral.

Borrowers are mainly miners and institutional OTC counterparties, with average transaction sizes from $1,000 to $500,000. This makes the model more controlled than unsecured lending: every loan is backed by BTC, and the company has a clear mechanism to protect the position if market conditions change.

Liquidity mechanics vary by plan. Full Flex and Flex holders can withdraw at any time subject to the standard 24-hour processing hold. Fixed plan holders have no withdrawal right until maturity, with early exit available through support at the cost of all accrued interest. The platform currently runs over $60 million in TVL across 11,400 active users. Coinhold does not publicly disclose the distribution of assets across plan types or current reserve levels, which is consistent with industry practice ahead of audit and licensing completion.

Transparency is where the gap to category leaders is most visible. Ledn publishes quarterly Merkle Tree proof-of-reserves, and Nexo holds three years of SOC 2 certification. These set the current benchmark for verifiable disclosure in CeFi yield products. Coinhold has not yet published independently audited financial statements, and an external audit is in the planning stages alongside MiCA licensing and SOC 2 certification on the product roadmap. Once that work is completed, Coinhold's disclosure standards will sit alongside the most transparent operators in the category. Until then, the structural arguments around mining fee income and conservative LTV ratios are assessable from public information, but the deposit-side picture is not yet independently verified.

The Bottom Line

For miners already inside the EMCD ecosystem, Coinhold is a natural yield layer on existing balances without any additional custody step. For external depositors, the Flex plan's roughly 9% on USDT clears the most transparent audited alternatives at comparable liquidity terms. The Fixed 360-day plan at 14% has no direct equivalent among fully audited peers at accessible conditions, but it requires a one-year lock and a deposit threshold most retail users will not meet.

Coinhold occupies a distinct position in the crypto savings market. It is a yield product backed by an operating mining business with nine years of track record and a conservative over-collateralized lending model, with a portion of the rate funded by operational fee income rather than deposit redeployment. The pending external audit and regulatory licensing will close the disclosure gap to category leaders. Until that work is done, the product's structural advantages are reasoned from public information rather than independently verified.