A look at Bitcoin vs. the $156 trillion global payment industry

Share:

Predictions Markets

See what traders are focused on

With the advent of new technologies built on top of the Bitcoin Network, Bitcoin’s use case for payments has expanded. However, why has business and consumer implementation of payments been so slow to date? What has been constructed, and what is lacking?

The cross-border payments industry is expanding rapidly and consistently, but incumbents in all segments lack incentives to substantially enhance the payments infrastructure. Their focus is on profit competition, which makes data sharing unattractive and revenue decline a low priority.

No consumer-facing or business-facing financial institution owns the underlying infrastructure, making it too easy for customers to avoid responsibility.

The cross-border payment industry

In 2023, it is possible to convey information to 86% of the world’s population almost instantly: through smartphones. However, transmitting money to anyone still takes days and costs an average of 6.24%. According to EY, in 2022, a projected $155.9 trillion will be transported abroad, up from $127.8 trillion in 2018. Other research institutions present contradictory information about this enigmatic sector.

The cross-border payments sector is expanding rapidly and steadily, yet incumbents in all segments lack incentives to significantly upgrade the underlying payments infrastructure.

According to the report, 78.8% of remittances, or $626 billion in 2022, went to low- and middle-income regions. Money transfers take days and cost 6.24% on average for remittances. This might theoretically drop to 3.31% if all consumers were completely aware of their options.”

According to The Global Findex Database 2021, worldwide adult ownership of financial accounts has increased from 51% in 2011 to 76% in 2021, and an estimated 10% of the global population does not have a government-issued ID to open an account.

Cross-border payment innovation is currently focused on two major initiatives:

1) the international integration of national instant payment systems and

2) the development of Central Bank Digital Currencies (CBDCs).

CBDCs receive little consideration inside the business for the enormous threat they pose in the hands of oppressive regimes seeking to target, punish, tax, and financially control specific segments of the population. According to Our World in Data, such totalitarian regimes house 70% of the world’s population. There is no regulation in place, nor are there any features that would preclude CBDCs from being used to impose government policies.

The global Bitcoin adoption

There are around 800,000 active Bitcoin addresses per day, although this is not an exact reflection of the number of daily users due to the technical nature of Bitcoin. According to Glassnode, there are approximately 32.9 million active entities in Bitcoin and approximately 44.4 million addresses with usable balances.

Moreover, as of June 2023, there are approximately 2.34 million bitcoin stored on 20 major exchanges. 500k BTC is on Coinbase, and 630k BTC is on Binance. These exchanges are currently under the SEC investigation. On all exchanges worldwide, analysts estimate a range of 48.8 – 97.5 million Bitcoin holders.

There is a significant overlap between the 32.9 million active entities and exchange users, as an estimated 70% of users store Bitcoin on exchanges and 80% in mobile or desktop wallets.

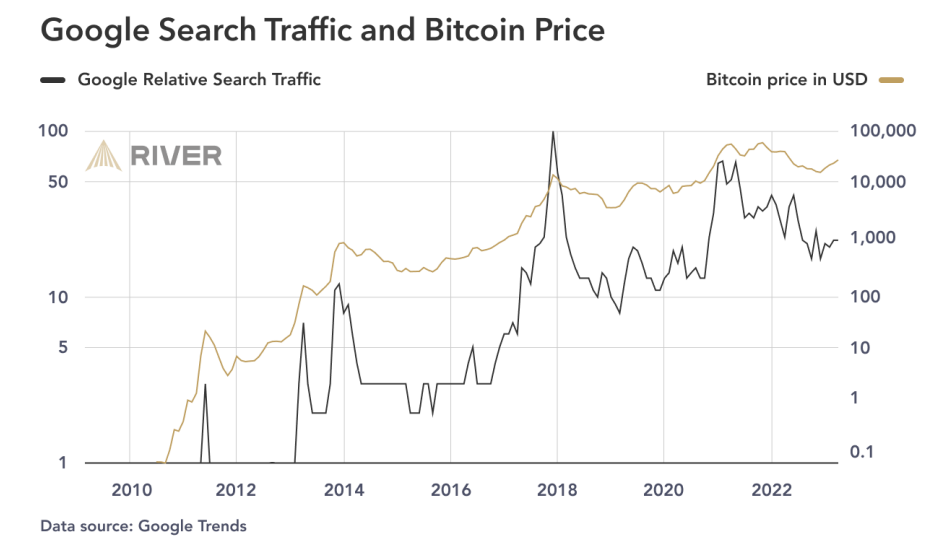

From 2013 to 2023, the relative Google search volume for Bitcoin was highest in Nigeria and El Salvador, where the average search query was nearly twice as likely to be about Bitcoin than in Austria, The Netherlands, and Switzerland.

Finally, globally, the number of individuals sending remittances (200 million) could be 100 to 400% greater than the number of Bitcoin holders.

Bitcoin cross-border payments

Bitcoin B2B cross-border payments remain unused at present. Generally, B2B is the last to embrace new technologies. It is perceived as a challenge to not only integrate the technology but also educate many different parties.

89% of consumers do not use Bitcoin for transactions and instead hold it for profit. The taxation regulations that transform Bitcoin transactions into taxable events discourage U.S. consumers from using Bitcoin.

From January to May of 2022, El Salvador’s central bank reported that Chivo Wallet processed $52 million in remittances or 1.6% of its estimated total volume of $3,175,000,000,000. Given Bitcoin’s relative novelty, this number is relatively significant.

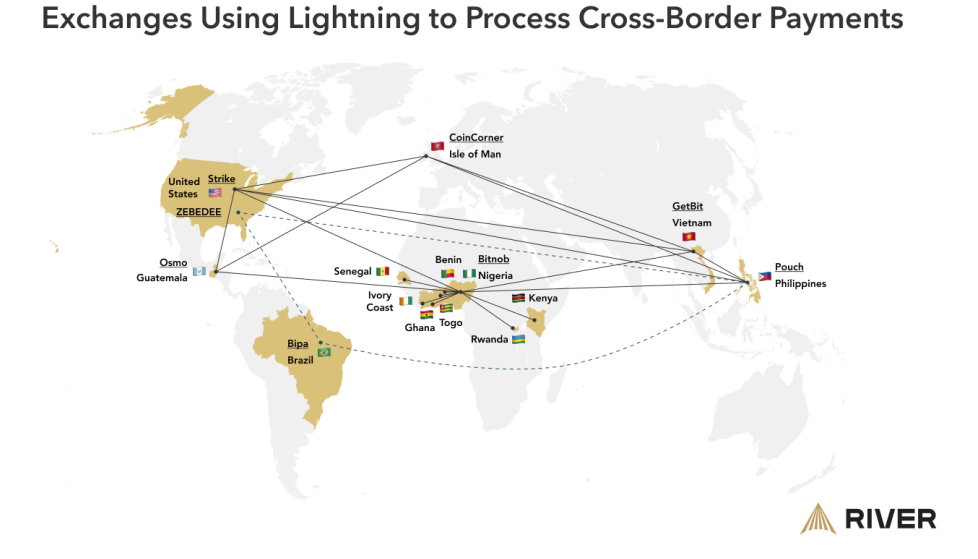

As described in the report, six companies on five continents have begun constructing payment networks using Lightning as the back-end infrastructure as of late 2022. In the future years, market analysts expect additional institutions to join them.

BTC proponents have a great deal of work and self-reflection to do if they intend to educate those who are currently uninterested in BTC. These advocates must explain BTC in a manner that resonates with the particular listener rather than from a general or subjective standpoint.

In addition, they must acquire additional learning experiences via articles, books, and podcasts. Lastly, they must target individuals who are already aware that fiat currency is flawed:

1. 2.5 billion people in 54 countries live with double-digit inflation.

2. Countries that heavily rely on remittances.

3. Countries with capital controls and black markets for currency.

Over the years, many efforts have been undertaken to increase BTC’s use in international transactions. Adoption is presently low in absolute terms, as Bitcoin’s primary function is not as a medium of exchange. As the world learns more about Bitcoin’s function as a store of value, the majority of users still prefer to hold their Bitcoins.

Despite this, B2C, C2B, and C2C cross-border payments adoption has been steadily increasing, and there are a number of legitimate use cases in which people around the world rely on Bitcoin for payments.

In This News

Coins

$ 72.93K

-2.98%

$ 0.00...361

$ 0.000734

$ 0.00391

$ 0.003

Predictions Markets

See what traders are focused on

Share:

In This News

Coins

$ 72.93K

-2.98%$ 0.00...361

$ 0.000734

$ 0.00391

$ 0.003

Predictions Markets

See what traders are focused on

Share:

Read More

Bitcoin Price Falls 5.5% in 5 Days to Below 73,000 as Spot ETF Outflows Accelerate