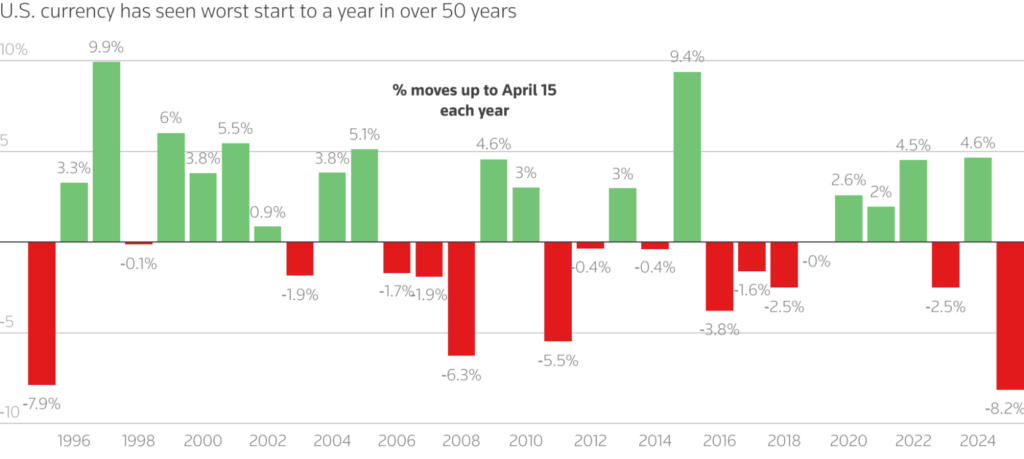

De-Dollarization: Goldman Sachs Warns U.S. Dollar to Drop 10% by April 2026

The U.S. dollar drop Goldman Sachs recently predicted is actually sending some serious ripples through financial markets. According to the investment bank, the U.S. dollar is forecast to decline about 10% against the euro and also roughly 9% against both the Japanese yen and British pound over the next 12 months. This assessment comes amid rising trade tensions and various policy uncertainties that are currently affecting global currency dynamics.

Also Read: De-Dollarization: 9 Countries Ditch the US Dollar

US Dollar Weakness: Key Drivers, Forecasts & Impacts on Global Markets

Tariffs and Currency Impact

US tariffs’ impact on the dollar is becoming increasingly evident as trade policies continue to shift. Goldman Sachs highlights how these changes are currently eroding both consumer and business confidence in multiple ways.

Michael Cahill, Goldman Sachs senior currency strategist, stated:

“We have previously argued that the US’s exceptional return prospects are responsible for the dollar’s strong valuation. But, if tariffs weigh on US firms’ profit margins and US consumers’ real incomes, they can erode that exceptionalism and, in turn, crack the central pillar of the strong dollar.”

The U.S. dollar drop Goldman Sachs predicts is linked to the changing nature of tariffs at this time. With broad tariffs affecting multiple countries, the dynamics are shifting dramatically in recent weeks.

Also Read: Pi Network: How to Be a Millionaire at $2.10 by 2025 & Beyond

Cahill writes:

“With broad and unilateral tariffs now on the table, there is less incentive for foreign producers to provide any accommodation. US businesses and consumers become the price-takers, and it is the dollar that needs to weaken to adjust if supply chains and/or consumers are relatively inelastic in the short term.”

Global Currency Shifts

Global currency fluctuations are being influenced by changing perceptions of U.S. governance and institutions. For almost a decade, the U.S. dollar benefited from significant capital flows into U.S. assets from developed market economies such as the euro area, Japan, and also Norway. This positioning is now expected to reverse in the coming period.

Signs of this reversal are already emerging. Consumer boycotts of U.S. goods have been observed, and reduced tourism flowing to the U.S. has been noted, with foreign arrivals to major U.S. airports falling following recent tariff announcements.

International Response to Dollar Weakness

The USD weakness forecast has prompted various responses from international financial institutions and governments. Foreign officials have taken several actions to attempt to reduce their reliance on the dollar, contributing to the U.S. currency’s declining share of foreign exchange reserves over the last decade.

Cahill notes:

“Up to now, private sector investors have more than compensated for reduced official sector demand, likely lured by superior asset returns. It is possible that the broader policy disruptions and eroded exceptionalism will see private sector investors follow a similar pattern now.”

Critical Import Challenges

The Goldman Sachs report highlights how critical imports, which are quite difficult to substitute, present additional challenges. With increased foreign pricing power, U.S. terms of trade may need to adjust via higher import costs, causing the dollar to depreciate rather than foreign currencies.

Also Read: Stocks and Dollar Crash Together—History Says ‘Tread Carefully’ in This Rare Situation

Cahill describes this situation as:

“Far from guaranteed, but it is newly possible with a 10% across-the-board tariff affecting every country outside the US.”

The U.S. dollar drop Goldman Sachs predicts appears increasingly likely to materialize as stronger-than-expected foreign spending plans combine with weaker U.S. asset performance. This has already led to some brief but active rotation out of U.S. assets and increased interest in hedging U.S. dollar exposure. The USD weakness forecast points to significant implications for global markets and also investors worldwide in the coming year.

Read More

De-Dollarization: Goldman Sachs Warns U.S. Dollar to Drop 10% by April 2026

The U.S. dollar drop Goldman Sachs recently predicted is actually sending some serious ripples through financial markets. According to the investment bank, the U.S. dollar is forecast to decline about 10% against the euro and also roughly 9% against both the Japanese yen and British pound over the next 12 months. This assessment comes amid rising trade tensions and various policy uncertainties that are currently affecting global currency dynamics.

Also Read: De-Dollarization: 9 Countries Ditch the US Dollar

US Dollar Weakness: Key Drivers, Forecasts & Impacts on Global Markets

Tariffs and Currency Impact

US tariffs’ impact on the dollar is becoming increasingly evident as trade policies continue to shift. Goldman Sachs highlights how these changes are currently eroding both consumer and business confidence in multiple ways.

Michael Cahill, Goldman Sachs senior currency strategist, stated:

“We have previously argued that the US’s exceptional return prospects are responsible for the dollar’s strong valuation. But, if tariffs weigh on US firms’ profit margins and US consumers’ real incomes, they can erode that exceptionalism and, in turn, crack the central pillar of the strong dollar.”

The U.S. dollar drop Goldman Sachs predicts is linked to the changing nature of tariffs at this time. With broad tariffs affecting multiple countries, the dynamics are shifting dramatically in recent weeks.

Also Read: Pi Network: How to Be a Millionaire at $2.10 by 2025 & Beyond

Cahill writes:

“With broad and unilateral tariffs now on the table, there is less incentive for foreign producers to provide any accommodation. US businesses and consumers become the price-takers, and it is the dollar that needs to weaken to adjust if supply chains and/or consumers are relatively inelastic in the short term.”

Global Currency Shifts

Global currency fluctuations are being influenced by changing perceptions of U.S. governance and institutions. For almost a decade, the U.S. dollar benefited from significant capital flows into U.S. assets from developed market economies such as the euro area, Japan, and also Norway. This positioning is now expected to reverse in the coming period.

Signs of this reversal are already emerging. Consumer boycotts of U.S. goods have been observed, and reduced tourism flowing to the U.S. has been noted, with foreign arrivals to major U.S. airports falling following recent tariff announcements.

International Response to Dollar Weakness

The USD weakness forecast has prompted various responses from international financial institutions and governments. Foreign officials have taken several actions to attempt to reduce their reliance on the dollar, contributing to the U.S. currency’s declining share of foreign exchange reserves over the last decade.

Cahill notes:

“Up to now, private sector investors have more than compensated for reduced official sector demand, likely lured by superior asset returns. It is possible that the broader policy disruptions and eroded exceptionalism will see private sector investors follow a similar pattern now.”

Critical Import Challenges

The Goldman Sachs report highlights how critical imports, which are quite difficult to substitute, present additional challenges. With increased foreign pricing power, U.S. terms of trade may need to adjust via higher import costs, causing the dollar to depreciate rather than foreign currencies.

Also Read: Stocks and Dollar Crash Together—History Says ‘Tread Carefully’ in This Rare Situation

Cahill describes this situation as:

“Far from guaranteed, but it is newly possible with a 10% across-the-board tariff affecting every country outside the US.”

The U.S. dollar drop Goldman Sachs predicts appears increasingly likely to materialize as stronger-than-expected foreign spending plans combine with weaker U.S. asset performance. This has already led to some brief but active rotation out of U.S. assets and increased interest in hedging U.S. dollar exposure. The USD weakness forecast points to significant implications for global markets and also investors worldwide in the coming year.

Read More